Why "Default Alive" Isn't Enough Anymore For SaaS and AI Startups?

2 mins

A few years ago, being "default alive" was an elite signal. When Paul Graham coined the term, it forced founders to face a brutal reality most were ignoring: burn, runway, and the mathematical proximity to zero. If you could prove your company would hit profitability before the bank hit empty, you were already ahead of the curve.

We have watched founders walk into rooms with that answer locked in — runway sorted, burn under control, growth trending right — and still struggle to articulate why the business deserves to win. Because "default alive" never answered that question. It only answered whether you would stick around long enough to figure it out.

The bar has moved significantly, and investors are no longer impressed by survival alone. They are evaluating how you operate while surviving. We have seen founders who are technically default alive quietly misallocating their best people, spreading themselves thin across decisions that do not matter, and slowly losing ground in their market. The cash is fine. Everything else is leaking.

Default alive tells you if you last, but it says nothing about whether you are building something worth lasting for.

The Market Changed. The Way Founders Think About Capital Didn't

Between 2020 and 2022, capital was cheap and easy. Founders raised on narratives, growth was the only metric that mattered, and "we'll figure out the unit economics later" was an actual strategy. In that world, being default alive put you ahead of most.

Then the conditions that made that strategy viable stopped working entirely.

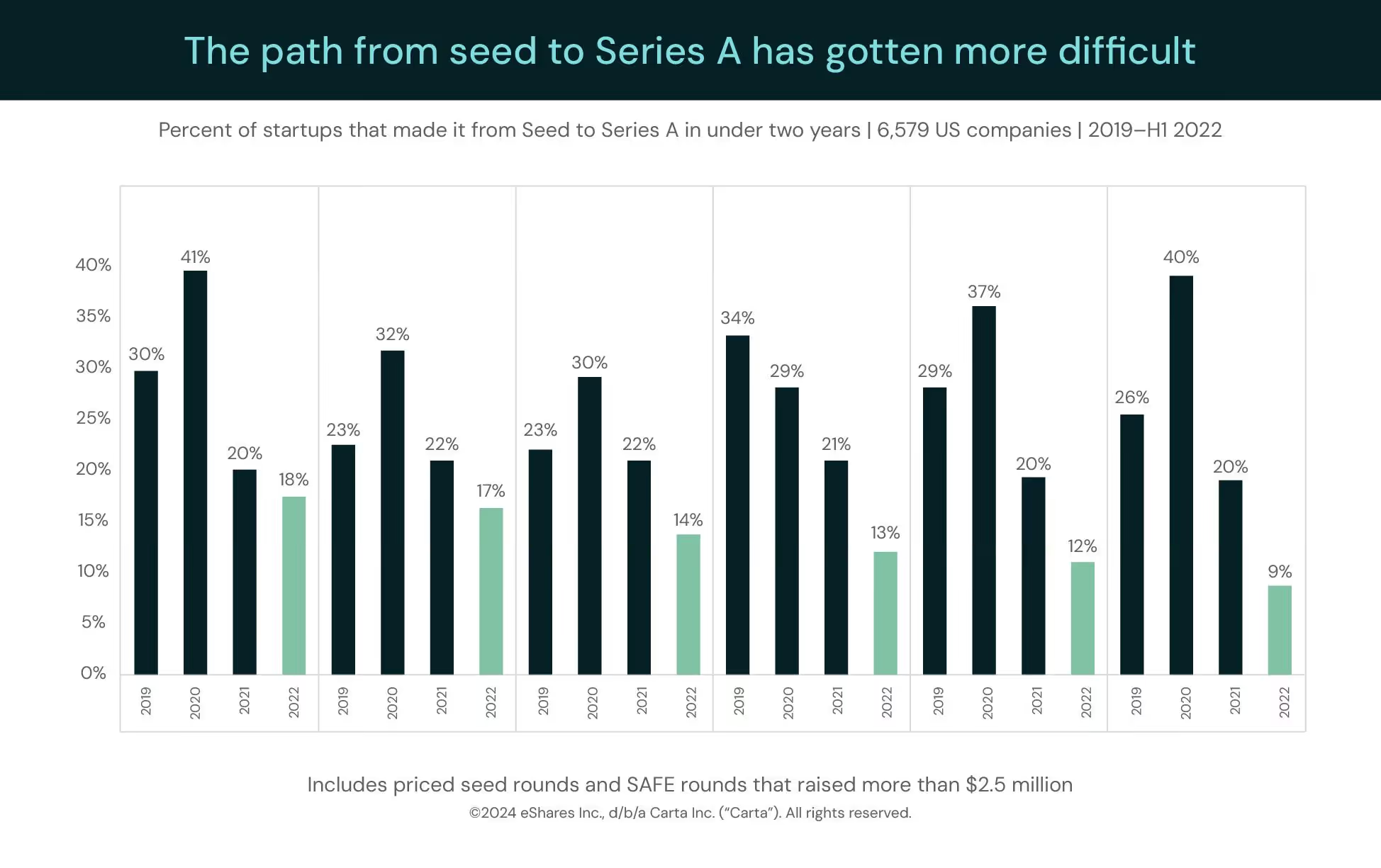

Rates climbed, LP patience ran out, and the numbers told a stark story. According to Carta's data, only around 14% of startups that raised seed in H1 2022 made it to Series A. That 14% isn't just a sign of a 'tough market.' It's a sign that the bridge between Seed and Series A is no longer built on growth alone; it's built on operating density.

Investors did not just get pickier, they started asking a fundamentally different question. Not "are you growing?" but "how intelligently are you operating while you grow?"

Most founders responded by getting tighter on spend, which was the right instinct. Cutting burn is still a survival move though, and it only helps you last longer. Lasting longer stopped being enough, because there is a significant difference between a stable bank account and a genuinely focused company.

What hasn't changed as much is how founders think about capital itself.

Take BigVU, for example. The company had real traction and growing usage, but like many SaaS businesses, it was constrained by how capital was structured. Delayed revenue cycles created cash flow pressure. To compensate, the company relied on expensive debt, which reduced flexibility and made growth harder to sustain.

Instead of continuing down that path or raising equity, BigVU restructured its capital approach using non-dilutive financing to stabilize cash flow, pay off high-cost debt, and reinvest into growth.

The outcome wasn't just an extended runway. The company reached breakeven and unlocked more efficient growth.

The gap we keep seeing is founders who are default alive but still running the business like survival is the goal. The financials look fine, but where the team's time is actually going, what the founder is focused on, and how the company sits in the market — that picture is usually a mess.

Default alive answers "will we make it?" The market is now asking "are we building something worth backing?" Those are different questions, and right now only one of them actually matters.

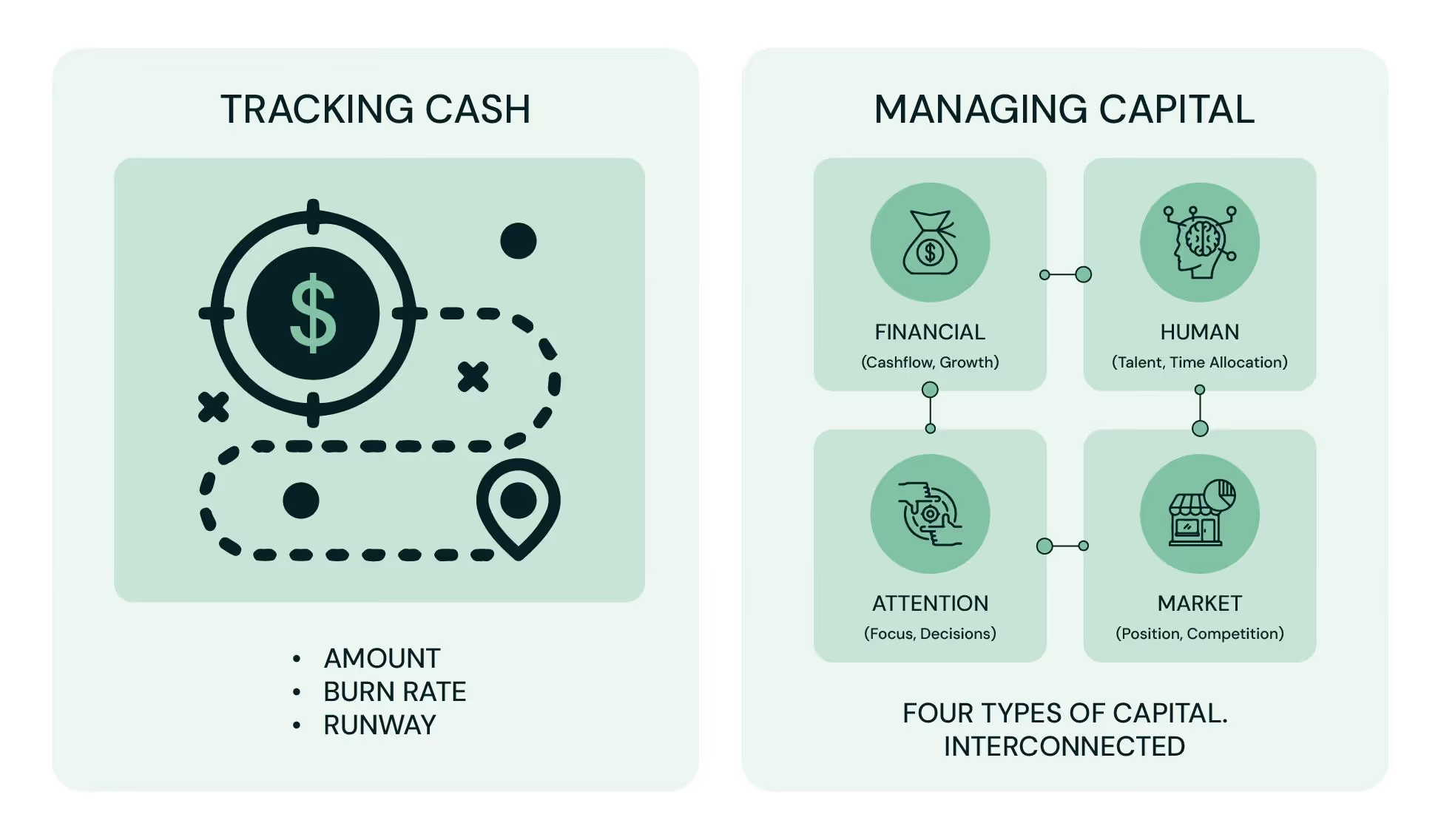

You're Tracking Cash. But Are You Managing Capital?

Most founders think they are managing capital, but what they are actually doing is tracking cash. There is a meaningful difference between the two.

Tracking cash tells you how much you have, how fast you are burning it, and roughly how long you have got. That information is necessary, but it is also just one perspective on one type of capital. Most businesses are running on four simultaneously.

Financial Capital

Financial capital is the one everyone watches. Metrics like burn rate, runway, and revenue growth live here, and founders tend to be honest about this one because the consequences of ignoring it are immediate and obvious.

Most founders track burn, runway, or revenue, but very few track return on capital deployed. To do this right, ask yourself:

- If I removed 30% of the spend today, what actually breaks?

- Which expenses are tied directly to growth outcomes?

- Where am I spending for activity vs results?

Signal you're doing it right: Every major expense is tied to a specific outcome or milestone.

Human Capital

Human capital is where most companies quietly lose their best ROI. The money is there, the people are there, and the output is not, because nobody is asking whether the allocation actually makes sense.

The issue is rarely talent. It's where that talent is applied.

Ask yourself:

- Are my top performers working on core growth levers?

- Is ownership clearly defined, or am I the bottleneck?

- Which roles are driving outcomes vs maintaining systems?

Signal you're doing it right: Your best people are working on your most critical problems.

Attention Capital

Attention capital is the one founders almost never talk about. A founder stretched across fifteen priorities is not leading the company, they are reacting to it. Unlike cash, attention does not show up on any dashboard until it is already gone. Every hour a founder spends 'playing' COO because they haven't optimized their human capital is a withdrawal from their Attention Capital. You can raise more money; you cannot raise more focus.

This is the most invisible and most mismanaged form of capital. Ask yourself:

- How much of my time is reactive vs strategic?

- What decisions can only I make, and am I focused on them?

- Where am I compensating for poor systems or unclear ownership?

Signal you're doing it right: Your time is concentrated on high-leverage decisions, not coordination.

Market Capitalization

Market capitalization is your external position. It reflects how the market sees you, how you are moving relative to competitors, and whether the ground you are standing on is getting stronger or slowly eroding. You can look perfectly stable on a spreadsheet while quietly losing competitive ground in ways that will not show up in your numbers until it is too late to correct. To avoid that, ask yourself:

- Why are customers choosing us today?

- Has that reason changed in the last 6–12 months?

- Are we winning on clarity or just pricing and speed?

Signal you're doing it right: You're gaining preference, not just customers.

Mismanaging all four is more common than most founders would admit. Here's a quick check:

- The company is default alive. Burn is controlled.

- But the three best people are working on the wrong things.

- The founder is in back-to-back calls that don't move the business.

- A competitor just closed two accounts that should have been yours.

If any of that sounds familiar, none of it will show up in your runway calculation, but all of it determines whether you win.

What Changes From Here

Default alive is still the mandatory starting line, and if you cannot answer whether your company makes it to profitability before the money runs out, that is the first problem to fix. Paul Graham's framework remains a useful forcing function for that question, but it was never designed to tell you whether you are making good decisions while you survive.

- Are the right people working on the right problems?

- Is your focus going where it actually moves the business?

- Will the market position you have today still hold twelve months from now?

Surviving with poor allocation is just a slower way to lose, and the founders who figure that out late rarely have the runway left to correct it.

The shift is not a complicated one, though it tends to be an uncomfortable one. Stop asking only "will we make it?" and start asking "are we deploying every form of capital we have with actual intention?" Most companies that did not make it were not killed by running out of cash. They were killed by misallocating everything else while the cash lasted, and by the time the damage showed up in the numbers, the options had already narrowed significantly.

The real question is not whether you are default alive. It is whether you are making the time it buys you count, or just watching it run out a little more slowly.

This is the gap Efficient Capital Labs works in, helping founders move beyond the survival question and into the operating one. If you are not sure how your capital is actually being deployed across the business, that is worth a conversation. Talk to us today!

Related posts

.avif)

The Invitation

Founders who drive the future deserve capital that accelerates with them. Let’s make this the most efficient chapter of your story.